Mutual funds operate in one of the most regulated sectors of the financial industry. Before an investor can invest, every fund house must complete Know Your Customer (KYC) verification to comply with anti-money laundering (AML), fraud prevention, and regulatory requirements. KYC involves collecting and verifying identity documents, address proof, PAN details, biometric information in some cases, and monitoring customer activity over time. As the mutual fund industry grows rapidly, especially in countries like India, the number of investors entering the market has increased dramatically. This has made KYC processing both a necessity and a major operational cost center. Because of this, an important strategic question arises:

Understanding the KYC Cost Problem

KYC is not a one-time activity. It is an ongoing compliance framework involving:

- Customer onboarding

- Identity verification

- PAN validation

- Address checks

- AML screening

- Risk profiling

- Record maintenance

- Periodic updates

- Regulatory reporting

- Data security management

- Fraud detection systems

All of these activities require:

- Technology infrastructure

- Compliance teams

- Cybersecurity systems

- Data storage

- APIs and integrations

- Audit mechanisms

- Vendor management

- Legal oversight

For large mutual funds handling millions of accounts, these costs can become substantial.

The challenge becomes even greater because KYC is largely a non-revenue-generating function. Investors do not invest in a mutual fund because its KYC department is stronger; they invest because of returns, trust, service quality, and brand reputation. Therefore, fund houses naturally seek ways to reduce compliance costs while maintaining regulatory standards.

What Does “In-House KYC” Mean?

An in-house KYC model means the mutual fund or its Asset Management Company (AMC) directly manages:

- Investor onboarding systems

- Verification workflows

- Data storage

- Compliance monitoring

- Regulatory reporting

- Technology infrastructure

- Customer document management

Instead of relying on centralized KYC utilities or third-party platforms, the AMC develops and controls its own KYC ecosystem.

This may include:

- Proprietary software platforms

- Internal compliance teams

- AI-driven fraud detection

- Integrated investor databases

- Direct API connections with regulators and government databases

Some very large financial institutions globally already maintain partially in-house KYC infrastructures because they have sufficient scale and resources.

Advantages of Solving KYC Internally

1. Greater Control

One of the biggest benefits of in-house KYC is operational control.

The mutual fund can:

- Customize onboarding flows

- Improve investor experience

- Modify verification rules quickly

- Integrate systems with internal CRM platforms

- Create faster approval processes

This flexibility can become a competitive advantage.

For example, a digital-first mutual fund platform may design a seamless paperless onboarding journey that reduces account opening time from days to minutes.

2. Better Customer Experience

In-house systems allow mutual funds to optimize every stage of the investor journey.

Benefits include:

- Faster account activation

- Personalized onboarding

- Better mobile app integration

- Reduced duplication

- Instant document verification

- Simplified user interfaces

A smoother onboarding experience can improve investor acquisition and retention.

3. Ownership of Investor Data

Investor data is highly valuable.

Managing KYC internally gives mutual funds:

- Full control over customer records

- Better data analytics opportunities

- Enhanced personalization capabilities

- Reduced dependency on third-party systems

Data ownership also supports:

- Cross-selling opportunities

- Risk assessment models

- Investor behavior analysis

- Targeted communication

4. Long-Term Automation Benefits

Once established, an advanced in-house KYC platform can automate many processes:

- AI-based document verification

- Facial recognition

- PAN matching

- AML alerts

- Fraud detection

- Risk categorization

Automation can gradually reduce manual processing costs.

Large AMCs with massive scale may eventually achieve operational efficiencies internally.

5. Enhanced Brand Trust

Some large financial institutions believe controlling compliance internally strengthens trust and accountability.

Investors may feel more comfortable knowing:

- Sensitive documents remain within the organization

- Data handling standards are internally supervised

- The AMC directly manages compliance responsibilities

The Major Challenges of In-House KYC

Despite these advantages, solving KYC entirely in-house is extremely difficult for most mutual funds.

1. Very High Initial Investment

Building a modern KYC infrastructure requires enormous upfront expenditure.

Key cost areas include:

Technology Development

- KYC software platforms

- Cloud infrastructure

- Cybersecurity systems

- AI verification engines

- API integrations

Compliance Teams

- AML specialists

- Legal experts

- Risk officers

- Audit professionals

Security Infrastructure

- Encryption systems

- Data protection frameworks

- Backup systems

- Fraud monitoring tools

Regulatory Integrations

- PAN databases

- Aadhaar verification systems

- CKYC systems

- Government APIs

The total investment can run into millions of dollars for a robust enterprise-grade system.

For smaller AMCs, this is financially impractical.

2. Continuous Regulatory Changes

KYC regulations evolve constantly.

Mutual funds must adapt to:

- New AML guidelines

- Updated SEBI regulations

- Data privacy laws

- FATCA compliance

- CRS reporting standards

- Digital onboarding norms

An in-house model requires continuous upgrades and compliance monitoring.

Failure to comply can result in:

- Heavy penalties

- Operational restrictions

- Reputational damage

- Legal liabilities

Regulatory maintenance itself becomes a recurring cost burden.

3. Cybersecurity Risks

Financial data is highly sensitive.

An internal KYC system creates major cybersecurity responsibilities, including protection against:

- Data breaches

- Identity theft

- Ransomware attacks

- Insider fraud

- Phishing attacks

- Unauthorized access

Cybersecurity spending is no longer optional.

Mutual funds must invest heavily in:

- Threat detection systems

- Encryption standards

- Security audits

- Incident response teams

- Penetration testing

For many AMCs, maintaining enterprise-level cybersecurity internally is extremely expensive.

4. Lack of Economies of Scale

This is perhaps the biggest problem.

KYC is fundamentally a scale-driven operation.

A shared utility spreads costs across:

- Multiple mutual funds

- Banks

- NBFCs

- Insurance companies

- Brokers

An individual AMC handles only its own investor base.

As a result:

- Per-investor cost remains high

- Infrastructure utilization is lower

- Duplication increases

For example, if 20 AMCs each build separate KYC systems, the industry collectively spends far more than if one centralized utility handles verification for all.

5. Duplication of Effort

Without a centralized framework, the same investor may complete KYC multiple times across different institutions.

This creates:

- Redundant documentation

- Operational inefficiency

- Customer frustration

- Higher processing costs

Centralized KYC utilities solve this duplication problem efficiently.

6. Operational Complexity

KYC operations require coordination across:

- Technology teams

- Compliance officers

- Customer support

- Regulators

- External vendors

Managing these internally increases operational complexity significantly.

Many mutual funds prefer focusing on:

- Fund management

- Distribution

- Investment research

- Investor servicing

rather than building large compliance infrastructures.

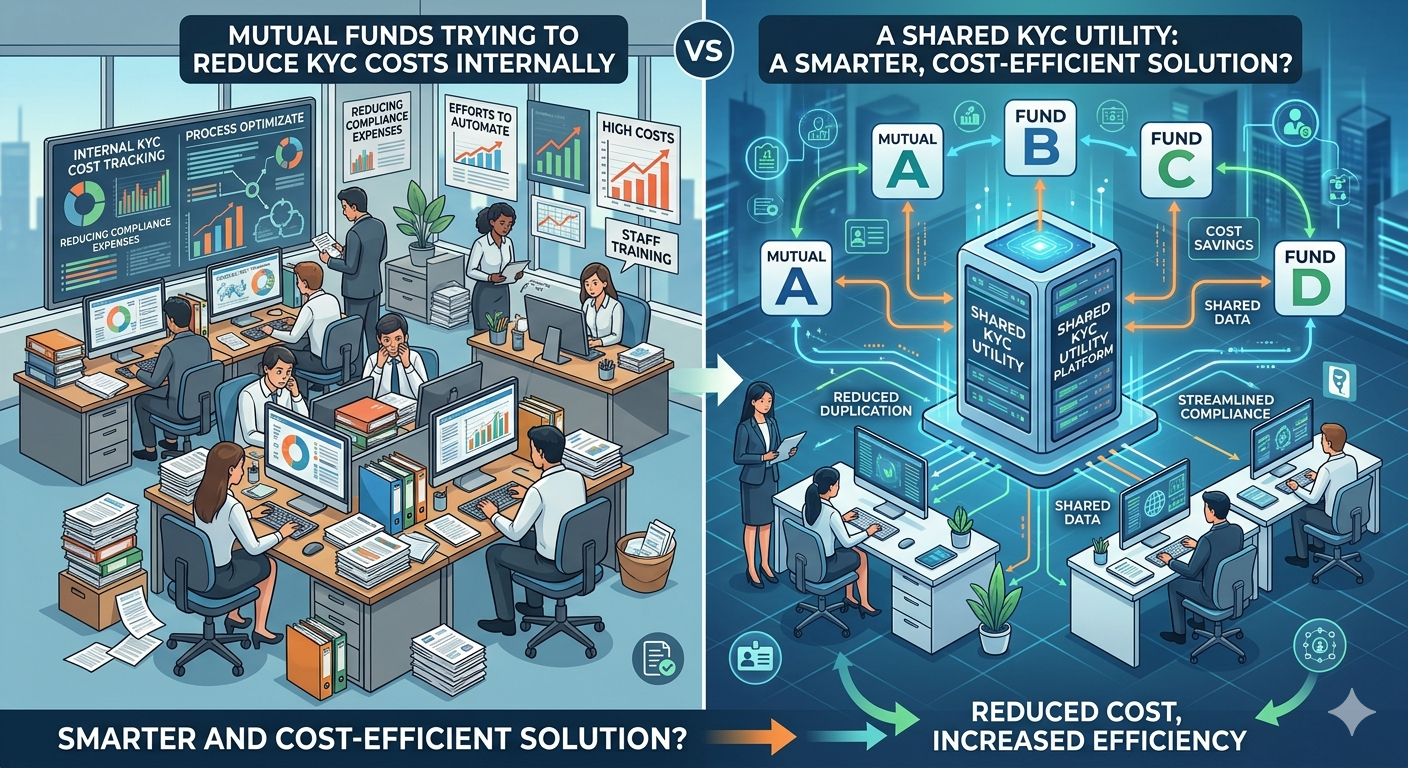

The Shared KYC Utility Model

A shared KYC utility is a centralized platform that performs KYC verification for multiple financial institutions.

In India, examples include:

- Central KYC Registry (CKYCR)

- KYC Registration Agencies (KRAs)

Under this model:

- Investors complete KYC once

- Multiple institutions access verified records

- Costs are distributed across participants

- Standardization improves efficiency

This model is increasingly becoming the preferred industry structure globally.

Why Shared Utilities Are Often Smarter

1. Massive Cost Reduction

The biggest advantage is economies of scale.

Shared utilities spread infrastructure costs across millions of users and hundreds of institutions.

This reduces:

- Per-investor processing costs

- Technology duplication

- Maintenance expenses

- Compliance overhead

The savings can be substantial.

2. Faster Standardization

Centralized systems ensure:

- Uniform KYC standards

- Consistent verification rules

- Standardized documentation

- Simplified audits

This improves industry-wide efficiency.

3. Better Regulatory Coordination

Regulators also prefer centralized systems because they:

- Simplify oversight

- Improve reporting

- Reduce fragmentation

- Enhance traceability

A shared utility can implement regulatory updates faster across all participants simultaneously.

4. Improved Investor Convenience

Investors benefit greatly from centralized KYC.

Instead of completing KYC repeatedly:

- One verification works across institutions

- Account opening becomes faster

- Documentation burden decreases

This improves financial inclusion and investor participation.

5. Superior Scalability

A centralized utility can scale more efficiently than individual AMCs.

Large platforms can invest in:

- AI systems

- Advanced cybersecurity

- Fraud analytics

- Automation technologies

at a scale individual mutual funds may not afford independently.

Are There Situations Where In-House KYC Makes Sense?

Yes — but mainly for very large institutions.

An in-house or hybrid model may work if a mutual fund:

- Has millions of investors

- Operates globally

- Requires specialized onboarding

- Wants premium customer experiences

- Has strong technology capabilities

- Can justify long-term infrastructure investments

Even then, most large institutions still combine:

- Shared KYC utilities

- Internal enhancements

- Proprietary workflows

rather than completely replacing centralized systems.

The Hybrid Model: The Most Practical Solution

Increasingly, the industry is moving toward hybrid KYC models.

In this structure:

- Core KYC verification is centralized

- AMCs add custom internal layers

For example:

- Shared utilities manage regulatory compliance

- Mutual funds manage customer experience internally

This allows AMCs to:

- Reduce costs

- Maintain flexibility

- Improve onboarding

- Avoid duplication

without bearing the full infrastructure burden.

The Role of Technology and AI

Technology is reshaping the KYC landscape dramatically.

Modern solutions now include:

- AI document verification

- Facial recognition

- Video KYC

- Blockchain identity systems

- Real-time fraud detection

- Digital identity wallets

Shared utilities can deploy these technologies more efficiently because of scale advantages.

Future KYC systems may become:

- Fully digital

- Real-time

- Interoperable

- Low-cost

- AI-driven

This further strengthens the case for centralized or hybrid models.

Strategic Perspective for Mutual Funds

Mutual funds must ask a key business question:

Is KYC a strategic differentiator or a necessary compliance utility?

For most AMCs:

- Fund performance matters more

- Distribution matters more

- Investor trust matters more

- Product innovation matters more

KYC is essential, but it is usually not the primary competitive advantage.

Therefore, spending excessively on standalone in-house KYC infrastructure may not generate proportional business value.

Conclusion

Mutual funds can technically solve their KYC cost problem internally by building in-house compliance and onboarding systems. Large institutions with strong financial resources, advanced technology capabilities, and massive investor bases may benefit from partial or hybrid internal solutions.

However, for most mutual funds, a fully in-house KYC model is neither the smartest nor the most cost-efficient approach.

The major reasons are:

- High infrastructure costs

- Constant regulatory changes

- Cybersecurity burdens

- Lack of scale economies

- Operational complexity

- Duplication of effort

Shared KYC utilities provide a far more scalable and economically efficient framework. They reduce industry-wide costs, simplify compliance, improve investor convenience, and enable better regulatory coordination.

As financial ecosystems become increasingly digital, the future likely belongs to hybrid models where:

- Centralized utilities handle core compliance

- Mutual funds focus on customer experience and innovation

Ultimately, the smartest strategy for most mutual funds is not to completely replace shared KYC systems, but to integrate intelligently with them while building selective internal capabilities where they create genuine competitive value.